Vinny Lingham, co-founder of Praxos Capital, told Unchained’s Laura Shin that Strategy’s financial structure is now unraveling in a way he predicted 18 months ago, and that the company may be approaching the point where every available move makes its position worse.

Vinny Lingham Predicted Saylor Would Hurt Bitcoin More Than FTX. Now He's Explaining Why

WRITTEN BY

SHARE

Key Takeaways

- Vinny Lingham predicted in October 2024 that Saylor would damage bitcoin more than FTX, with MSTR now down over 80%.

- Strategy holds $6.7B in convertible notes; Shin cites an analyst who estimates covering early maturities requires selling up to 74,000 BTC or more.

- Lingham says STRC, trading under $76, will never return to $100 par, and that Strategy’s cash runway is limited.

Lingham Called It Early

The co-founder of Praxos Capital, Vinny Lingham, once known as the “Oracle,” joined Laura Shin for an episode of the Unchained podcast that aired on June 25, 2026. At the outset of the interview, Lingham was quick to revisit a prediction he made two years earlier about Strategy, the bitcoin treasury company formerly known as Microstrategy.

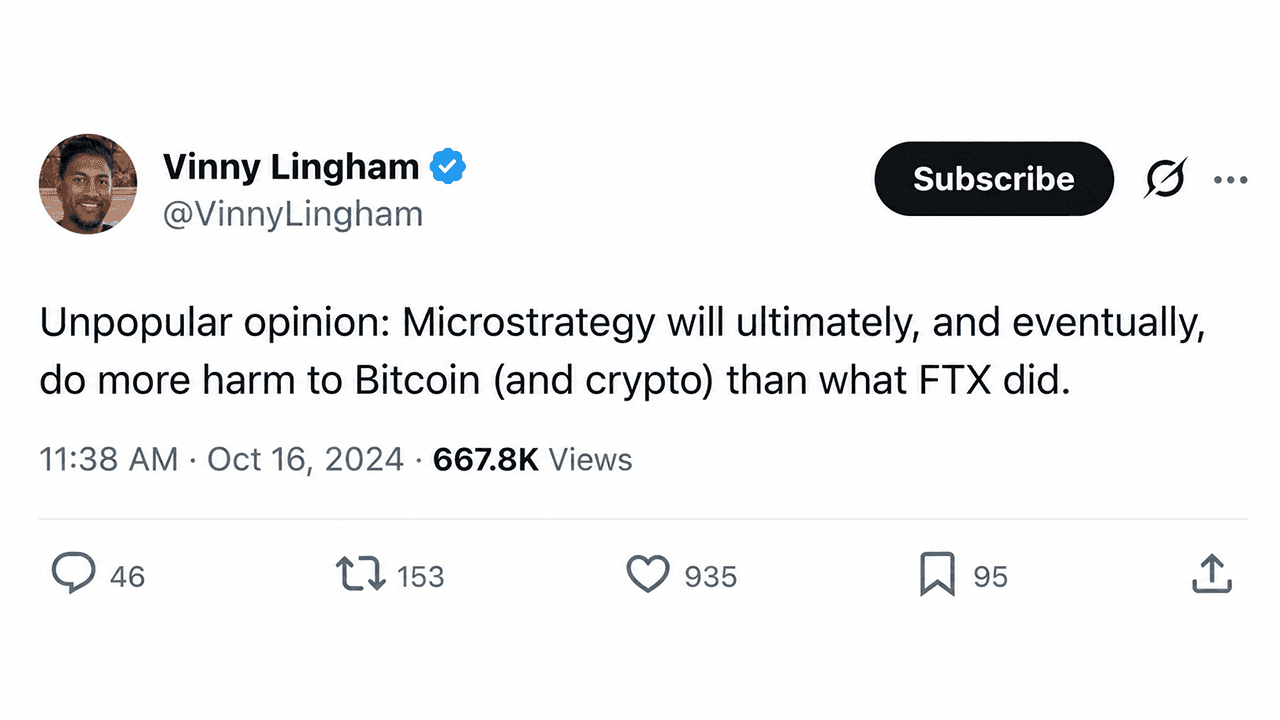

In October 2024, Lingham posted a warning on X that Michael Saylor would ultimately do more damage to bitcoin than FTX. The prediction drew mockery at the time. MicroStrategy was trading near its all-time high of $473.83. As of this week, MSTR has dropped more than 80% from that peak, trading around $90.70.

“I put out a tweet back in October 2024 saying that, ultimately, I believed Michael Saylor would do more damage to bitcoin than FTX,” Lingham explained during the interview with Shin.

He added:

“At the time, it was a very unpopular prediction. Now, 18 months later, people are starting to wonder whether I was actually right.”

The ‘Saylor Scheme’

Lingham stops short of calling Strategy a Ponzi scheme, but he has coined his own term for what Saylor built.

“He’s built an extremely complex capital structure consisting of debt and multiple layers of preferred securities,” Lingham argued “I jokingly call it a ‘Saylor scheme.’ He issued STRC, STRD, STRK … and several others. When one offering stopped working, he simply introduced another.”

STRC, one of the preferred share classes at the center of recent market concern, closed today at $75.69, after falling under $74 earlier this week. Lingham does not expect it to recover.

“I don’t believe STRC ever returns to $100,” he said. “I’d bet it never trades back at par again.”

The Chess Endgame

Strategy recently raised $335 million, selling 2.7 million shares of common stock and using roughly $300 million to build its cash reserves to approximately $1.4 billion. That cash is expected to cover preferred dividend obligations for about 10 months. In Lingham’s view, the market responded by continuing to sell both MSTR and STRC.

Lingham says the company’s recent move to bimonthly dividend payments made the situation worse. More frequent payment cycles mean management has less time to respond when conditions deteriorate, and each cycle tightens the pressure on cash reserves.

He describes Saylor’s current position using a term from chess.

“Michael is now in what’s known in chess as zugzwang,” Lingham said. “Every move available to him is a losing move. If he raises the dividend yield, he shortens his cash runway. If he issues more shares, he dilutes common shareholders further.”

The $6.7 Billion Debt Problem

During the discussion, Shin explained that Matt Walsh a founding partner of Castle Island Ventures, recently raised concerns about Strategy’s convertible notes, which total roughly $6.7 billion outstanding. Shin said the notes carry put rights that allow holders to demand cash repayment at par if the notes are not converted or refinanced. Walsh estimated that covering the first three maturities through June 2028, at a bitcoin price around $60,700, would require selling approximately 74,000 BTC. Covering the full schedule would require around 111,000 bitcoin.

Lingham responded to Shin’s summary of Walsh’s X post and insisted that the market is already pricing that risk in.

“Strategy sold just 32 bitcoin and the market reacted negatively,” he said. “Imagine what happens if the company eventually has to sell tens of thousands of bitcoin.”

The Reflexive Loop in Reverse

Lingham argues that Strategy’s aggressive accumulation created a self-reinforcing cycle that worked well on the way up. The company bought bitcoin, which he believes pushed the price higher, which increased MSTR’s value, which allowed it to issue more shares and buy more bitcoin. He now argues that the cycle is running in reverse.

“Once Strategy stops being the biggest buyer of bitcoin, selling pressure starts outweighing buying pressure,” he said. “Liquidity disappears. The largest source of demand is gone.”

He added that Strategy’s mNAV sitting around 1.06 is historically a level at which similar investment vehicles trade to a discount. He said a value closer to 0.90 would make more sense given the circumstances.

What Comes Next

Lingham told the Unchained podcast host that the healthiest outcome would be for Saylor to stop buying bitcoin, stop issuing new shares, preserve cash, and wait for a market cycle recovery. He does not expect that to happen.

“I don’t think he’ll admit that the strategy needs to change,” Lingham said. “I think hubris plays a significant role here.”