Christopher Giancarlo, former head of the CFTC, proposes that banks integrate and offer yield on stablecoins deposits to customers, avoiding the imbalances that worry the banking establishment. For him, this compromise would allow the Clarity Act to move forward, with benefits for both banks and crypto exchanges.

Former CFTC Chief Calls for Allowing Banks to Offer Yield on Stablecoin Deposits

WRITTEN BY

SHARE

Former CFTC Head Christopher Giancarlo Proposes Banks to Offer Yield on Stablecoins

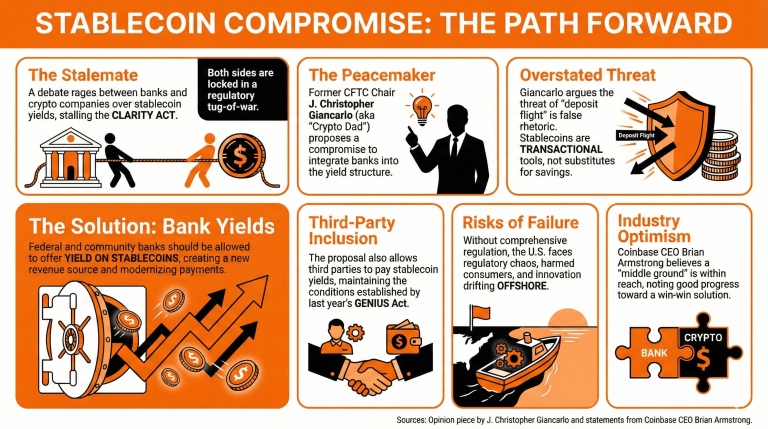

While the debate between banking institutions and crypto companies rages on regarding stablecoins and yield, some believe a middle ground can be reached.

Former Commodity Futures Trading Commission Chairman J. Cristopher Giancarlo, also known as “ Crypto Dad” for his positive stance on cryptocurrency and blockchain issues, believes that the current stalemate preventing the approval of the Clarity Act can be solved by integrating banks into the yield structure for stablecoins.

In a recent op-ed, Giancarlo stressed that the stablecoin threat was overstated, qualifying this take as rhetoric against this bill. He stated that there was no link between stablecoins and deposit flight, explaining that, for him, these were used as transactional and payment instruments rather than a substitute for already established savings tools.

Even so, Giancarlo proposed that federal banks, including community banks, could also offer yield on stablecoins, opening a path for a new revenue source and modernizing their payments infrastructure, an issue particularly relevant for smaller banks.

This proposal also includes allowing third parties to pay yield on stablecoin deposits, maintaining the conditions established by the GENIUS Act passed last year. The compromise would result in a win-win outcome for all parties, allowing the crypto industry to pass regulation and overcome the current stalemate.

Giancarlo also warned about the consequences of failing to pass comprehensive crypto regulation, stating that it would invite “regulatory chaos that harms banks and consumers alike, saps economic dynamism and forces innovation to drift offshore.”

“The Senate has the tools to resolve this impasse and to follow the strong leadership displayed by the White House. Failing to do so would be a choice, not an inevitability,” he concluded.

Brian Armstrong, CEO of Coinbase, recently declared that he was confident that a compromise would be reached, highlighting that they were making “good progress” towards a solution beneficial to all parties involved.

Coinbase CEO Confident of ‘Win-Win-Win’ Deal Between White House, Banks, Crypto

Coinbase is intensifying efforts to shape U.S. crypto market structure legislation as CEO Brian Armstrong pushes for a breakthrough between…

Read Now

Coinbase CEO Confident of ‘Win-Win-Win’ Deal Between White House, Banks, Crypto

Coinbase is intensifying efforts to shape U.S. crypto market structure legislation as CEO Brian Armstrong pushes for a breakthrough between…

Read NowCoinbase CEO Confident of ‘Win-Win-Win’ Deal Between White House, Banks, Crypto

Read NowCoinbase is intensifying efforts to shape U.S. crypto market structure legislation as CEO Brian Armstrong pushes for a breakthrough between…

FAQ

-

What proposal has J. Christopher Giancarlo put forward regarding stablecoins?

Giancarlo suggests integrating banks into the yield structure for stablecoins to resolve the current stalemate surrounding the Clarity Act. -

How does Giancarlo view the threat posed by stablecoins?

He believes the concerns about stablecoins causing deposit flight are overstated, emphasizing that they are primarily used for transactions rather than as savings alternatives. -

What benefits does Giancarlo’s proposal offer to banking institutions?

By allowing federal and community banks to offer yield on stablecoins, the proposal could provide a new revenue source and modernize payment infrastructures, particularly for smaller banks. -

What are the potential consequences of failing to pass comprehensive crypto regulation, according to Giancarlo?

He warns that without proper regulation, there could be “regulatory chaos” that harms both banks and consumers, leading to reduced economic dynamism and pushing innovation offshore.