Following the hack at Bitfinex, many people stand to lose money as the company spreads losses among users. A 36% haircut was announced, but some users claimed even bigger losses. American tax accountant Daniel Winters explains how the IRS could allow U.S. taxpayers to deduct their losses from the Bitfinex hack.

Loss of Bitcoins in Bitfinex Could be Deducted on US Tax Returns

This article was published more than a year ago. Some information may no longer be current.

WRITTEN BY

SHARE

Also read: Bitfinex ‘Leaning Towards’ Bail-In, Haircut for All BTC Traders

Tax Deduction for Bitfinex Hack Victims

Accountant Daniel Winters, founder of Global Tax Accountants LLC., has over 12 years of tax experience. He was previously employed by KPMG, Ernst & Young and Schonbraun McCann before starting his own business.His firm provides tax and accounting services to the blockchain space.

“It may be small consolation for the US users of Bitfinex, but IRS tax rules allow you to take a loss for the stolen Bitcoins,” he wrote in his blog post, and noted that:

For US persons reporting the loss on their tax return, the basic question is whether this will be a capital loss, or a theft/casualty loss.[…] Also, if Bitfinex provides partial reimbursement of losses, this will affect the loss calculation.

Attempting to explain to how to generally deduct bitcoin losses on US tax returns, Winters stressed that “The characterization of the loss has very different tax consequences.”

Specifically for the Bitfinex hack, Winters said that “since the Bitfinex hack was a theft, you may be eligible to deduct this is a theft/casualty loss, depending on your personal circumstances.” He cited that for customers in the business of trading with trader status, the treatment may be different and beyond the scope of his post.

Bitcoin is Property, Treated Like a Capital Asset

The IRS classifies bitcoin as property, so it is “generally treated  as a capital asset,” said Winters. Anyone selling bitcoin would report the sales on Schedule D, as they would the sales of other capital assets including stocks and bonds.

as a capital asset,” said Winters. Anyone selling bitcoin would report the sales on Schedule D, as they would the sales of other capital assets including stocks and bonds.

“If your capital losses are more than your capital gains, you can deduct the difference as a loss on your tax return,” according to the IRS website. However, the loss is limited to $3,000 per year, or $1,500 for married-filing-seperate-return taxpayers. “Unused capital losses are carried forward indefinitely,” Winters commented on Reddit.

How to Deduct Bitcoin Loss

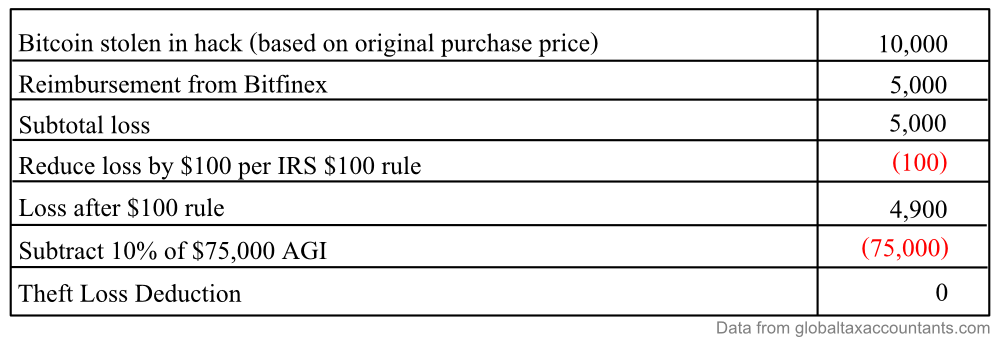

Winters went on to explain that only taxpayers who itemize their deductions on Schedule A and not using standard deduction can claim this deduction and “you can only deduct losses in excess of 10% of your adjusted gross income (AGI),” he said.

Additionally, he noted that since the bitcoins were stolen, it is equivalent to selling it at the price of zero. This means the “Capital loss = the original purchase price in USD, not the value at the time of the hack,” Winters explained. He gave an example, for taxpayers with an AGI of $75,000, there is nothing to deduct as shown below.

Winters concluded that for a taxpayer to take a deduction based on bitcoin losses, either the loss will have to be much larger or the income lower, or perhaps a combination of the two.

If a customer takes a loss in 2016 and then receives a reimbursement in 2017, Winters clarified that the amount received in 2017 would be considered income and must be reported on the tax return. The “IRS doesn’t allow double dipping,” he commented.

How many Bitfinex customers do you think can deduct their losses in the manner described above? Let us know in the comment section below.

Images courtesy of Twitter, IRS, globaltaxaccountants.com, washingtontimes.com