In the Tuesday edition of Bitcoin in Brief: low quality altcoins refuse to die, Coincheck hackers launder their last NEM, and what’s up with all the bitcoin bull traps? Welcome to your daily roundup of drama from the tumultuous world of crypto.

Bitcoin in Brief Tuesday: Breakouts and Fakeouts

This article was published more than a year ago. Some information may no longer be current.

WRITTEN BY

SHARE

Also read: Bitcoin in Brief Monday: Twitter Wields the Banhammer

Yet Another Bull Trap

There’s a pattern that’s become all too familiar for anyone who’s been watching the markets in recent weeks. After lingering around $6.7k territory for days, bitcoin will break out, soaring well over $7k and seeding hope that a recovery could finally be on. And then, almost as quickly as the green candle has materialized, it turns red and plummets back to where it started, ready to initiate the breakout/fakeout sequence all over again.

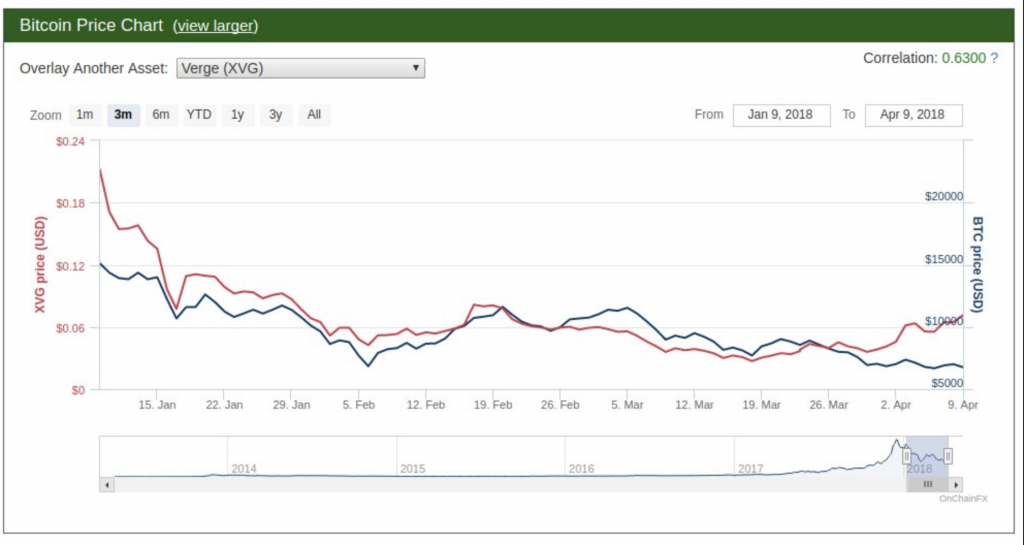

When altcoins crashed hard in mid January, it was believed that one upside would be that the vaporware projects – yes, shitcoins – would get found out and left behind. Instead, as Onchainfx notes, the likes of tron and verge have kept pace with bitcoin, and in fact the latter has outperformed BTC of late thanks to verge’s “big partnership” that’s to be announced on April 16. News. Bitcoin.com shall refrain from disclosing the name of verge’s new partner, but no, it’s not Amazon, and it isn’t Apple either, which may come as a disappointment to verge’s more fanatical supporters.

Coincheck Hackers Are All Out of NEM

Deepdotweb reports that Coincheck’s hackers have laundered the last of their NEM on the deep web. They’re believed to have raised over $100 million for the stolen coins, which they were offering for LTC or BTC at a discount. There’s a certain irony in the attackers setting up their very own crypto exchange to sell the coins they’d pilfered from Japan’s Coincheck exchange. Their next step is to launder the litecoin and bitcoin they’ve received which, compared to offloading the red-hot NEM, must feel trivial in comparison.

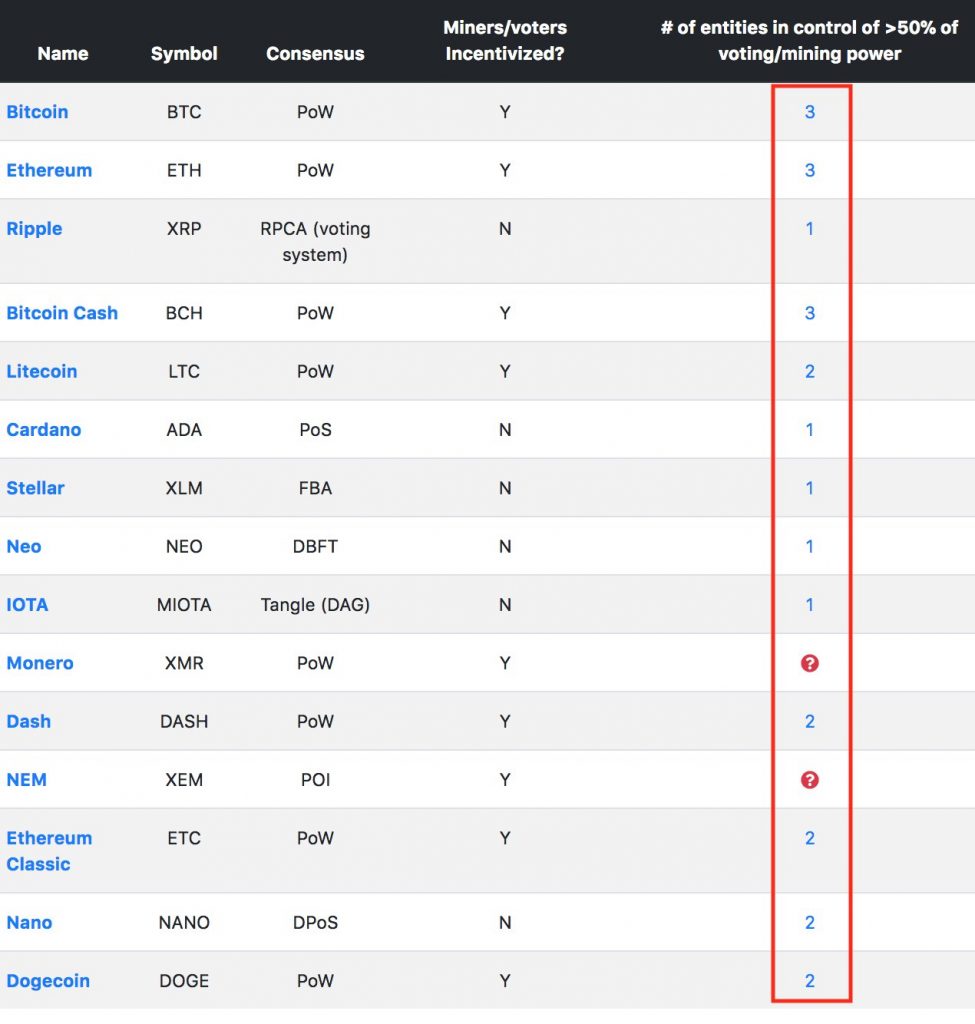

Centralization Is Inevitable

Nic Carter (who also runs Onchainfx, mentioned earlier in this article) has outlined The Palmer Principle, named after dogecoin’s Jackson Palmer: the notion that “no matter the consensus mechanism, in practice, 51% of stake/mining power will be owned by at most 3 entities.” ASIC-friendly algorithms or otherwise, mining pool domination is inevitable.

Do you think a handful of pools dominating crypto mining is inevitable? Let us know in the comments section below.

Images courtesy of Shutterstock, Onchainfx, and Deepdotweb.

Need to calculate your bitcoin holdings? Check our tools section.