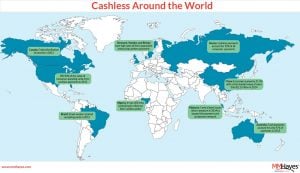

As Denmark and Sweden spearhead the move to a cashless society, the ramifications of such a transition for humanity as a whole could result in the exclusion of certain groups and classes.

A Cashless Society is Economic Apartheid (Without Bitcoin)

This article was published more than a year ago. Some information may no longer be current.

WRITTEN BY

SHARE

Also read: Bitcoin.com Sponsoring Scaling Bitcoin II in Hong Kong

100% Digital

A cashless society is one where people do not use physical cash; all purchases are made by credit cards, charge cards, checks or direct transfer from one account to another (e.g. Bitcoin, PayPal etc.). And while many would argue that most of world’s money is already in digital form — over 95% — we still need to completely eliminate physical cash and coins to enter the cashless era.

A cashless society is one where people do not use physical cash; all purchases are made by credit cards, charge cards, checks or direct transfer from one account to another (e.g. Bitcoin, PayPal etc.). And while many would argue that most of world’s money is already in digital form — over 95% — we still need to completely eliminate physical cash and coins to enter the cashless era.

“The Swedish central bank, Riksbanken, is working towards a goal to decrease cash in society and possibly to remove it entirely,” said Christian Ander of Stockholm-based BTCX to Bitcoin.com. “We also see more and more socially important services removing cash as a means of payment, commuting in Sweden is one example. Coffeehouses and restaurants are seeing increased costs with cash as most of the major banks stop accepting cash deposits throughout Sweden and only offer a few places where this can be done.”

It appears that a “war on cash” has been unofficially declared by banks, with the heaviest assault taking place currently in countries like Italy, Spain, France, UK and the US, in addition to the aforementioned Scandinavian nations. For example, Spain has already banned cash transactions of more than 2,500 EUR; Italy has banned cash transactions of more than 1,000 EUR.

Economic Apartheid in Disguise

Ironically, the usage of money in digital form creates a physical barrier between digital currency and people through exclusion. Take a closer, look and this becomes a tacit policy of de facto economic apartheid, accommodating only the “banked,” or only those people with the means to access the traditional banking system.

Ironically, the usage of money in digital form creates a physical barrier between digital currency and people through exclusion. Take a closer, look and this becomes a tacit policy of de facto economic apartheid, accommodating only the “banked,” or only those people with the means to access the traditional banking system.

Everyone else below a certain income threshold and without access to banking for whatever reason will be relegated into the underground economy by default, along with money-launderers and criminals.

Ander says:

“It’s an extremely bad idea to remove cash entirely from the society; it enables mass surveillance from both the payment industry and the government. Where and what you spend your money on is a right to privacy much similar to what you vote for.”

“It’s a potential threat to a democratic society when you cannot pay your member fee to a political party, religious belief or any other membership organization without risking surveillance and in worst case, your life,” he adds.

Moreover, physical currency enables direct, peer-to-peer exchange, whereas debit cards, for example, involve a series of intermediaries. In other words, a cashless society will involve a middleman in every transaction; whether you give a dollar to a homeless person or borrow a few bucks from a friend, there will be a financial entity in between — watching your every move.

Enter Negative Interest Rates

Alongside the push to eliminate cash is another interesting phenomenon that’s currently transforming the economic landscape: zero and negative interest rate policies (ZIRP, NIRP). Negative rates mean that banks literally pay businesses and people to borrow money while penalizing savers for “hoarding” it.

Alongside the push to eliminate cash is another interesting phenomenon that’s currently transforming the economic landscape: zero and negative interest rate policies (ZIRP, NIRP). Negative rates mean that banks literally pay businesses and people to borrow money while penalizing savers for “hoarding” it.

“Over the past 30 years, however, world real (i.e. adjusted for inflation) interest rates have been in secular decline,” explains Andrew Haldane, the Bank of England’s chief economist. “At the dawn of the crisis, they had halved to around 2%. Since then they have fallen further to around zero, perhaps even into negative territory.” Haldane warns that low interest rates may actually be a permanent feature of the monetary system, which begs the question: can banks tax customer deposits and savings accounts?

Yes, if you eliminate all physical cash.

This way, all money can then be centrally controlled and thus subject to unfair taxation, inflationary measures and all other types of manipulation that Keynesians can only dream of. However, the implementation of such a radical policy will require some shock to the current system, according to the president and founder of Pento Portfolio Strategies, Michael Pento.

“Strategies such as pushing interest rates into negative territory, outlawing cash, and sending electronic credits directly into private bank accounts may appear more palatable in the midst of market distress,” notes Pento.

Moreover, Fed Chair Janet Yellen also admitted to “new policy tools” being on the table for fighting deflationary pressures.

“Policymakers have to carefully weigh the advantages and disadvantages of alternative monetary implementation frameworks in the presence of new policy tools,” Yellen said last week at a two-day research conference sponsored by the Fed.

It appears that the last days of cash will come amid some future “market distress” (which is guaranteed in our boom-bust cyclical economy), alongside the introduction of NIRP, essentially transferring total control over all money to the incumbent banking system.

Digital Currencies vs. Cryptocurrencies

As money transitions from physical to digital form and people increasingly become accustomed to using “digital currency units,” banks and the mainstream media will continue to ignore the taboo question of who should have control of money. This is the important distinction between digital currencies (e.g. debit card, ApplePay) versus cryptocurrency, i.e. digital currency units secured cryptographically, which means that only the holder of the private keys can use it.

“Ownership is nine tenths of the law; but with bitcoin, ownership is ten tenths of the law,” explains Andreas Antonopoulos in his book, Mastering Bitcoin.

So with cash gone and banks charging people money simply for “having” it, it’s reasonable to assume that people will seek out all possible ways to preserve their savings. So then what? Gold? Perhaps, but gold could be confiscated and made illegal with the stroke of a pen as happened in the US during the 1930s, coincidentally also during “times of distress.”

So if not precious metals, could cryptocurrencies such as bitcoin become a viable alternative?

Ander:

“The blockchain could possibly replace cash to offer both privacy and transparency, leaving us with a dependency with internet and mobile devices to conduct financial transactions. This is however an interesting scenario, and more likely to be an option rather than removing cash all together.”

Since the price of smartphones is expected to keep falling — and can already be bought for as little as $10 USD — enabling virtually everyone to access the internet, decentralized cryptocurrencies can indeed become a formidable counterbalance to the financial system’s hegemony.

Therefore, as cash is systematically phased out going forward, its independent spirit may only be preserved if converted to bitcoin, for example. Because if one cannot stuff digital currency under a mattress — or secure it cryptographically as with cryptocurrencies — then who ultimately has control of your money in the future cashless society?

The answer becomes obvious.

What do you think of a cashless society? Let us know in the comments below!

Images courtesy of Getty Images, mmhays

{kind=link}